[ad_1]

Damirkudic

by Valentum analysts

The trend towards a cashless society is inevitable, and there are a number of companies where one can gain exposure to this dynamic, but our favorite is Visa (NYSE:V). Many investors know Visa A credit card company, but its business model is a little different than expected. For example, Visa charges a fee every time someone uses one of its cards, and avoids the credit risk that can complicate other operators’ business models. We really like this one. Because the exposure rate of visa is greatly reduced.

Another amazing feature of Visa is its huge profitability. Visa, for example, maintains operating margins and free cash flow margins that are as strong, if not stronger, than any other company in our coverage universe. We are talking about operating margins north of 60% and free cash flow. With flow margins of nearly 50%, these levels of profitability are incredible. Not only is the firm’s income statement rich, but the firm’s free cash flow is rich. He doesn’t need to put a lot of working cash flow back into the business to keep things moving in the right direction.

Visa’s latest quarterly results

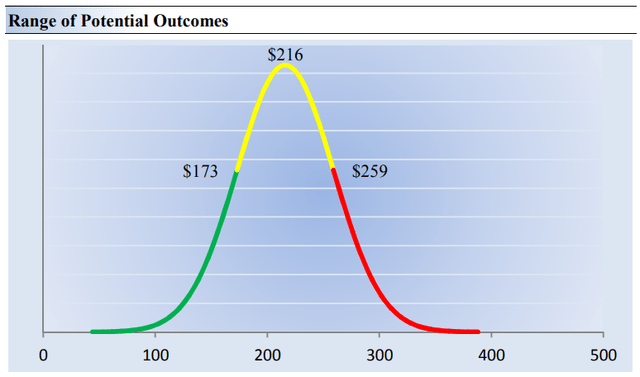

Let’s see how things have been in Visa lately. The company reported impressive first quarter fiscal 2023 results on January 26. Sales grew 12 percent in the period, and Visa attributed that top-line expansion to a 17 percent increase in non-GAAP revenue. The company’s quarterly operating margin was a strong 64.1%, a rebound from the prior-year quarter’s level but still impressive. Visa’s non-GAAP earnings per share rose 21 percent, to $2.18, coming in better than consensus expected. Visa shares have jumped nearly 10% in the new year, and while the company’s stock price exceeds our point estimate of its intrinsic value, we could see shares reach a high of $259 per share. , in our view.

Our fair value estimate range for Visa shares. (Image Source: Valuentum)

As we noted above, Visa is not as exposed to credit risk as other credit card companies, so delinquencies and charges against entities such as Discover Financial ( DFS ) and Capital One Financial ( COF ) are expected to increase materially. , Visa is mostly protected from credit risk in this regard. It is charged every time the card user takes out a Visa card, not on the interest charged on the balance itself. In the first quarter of fiscal 2023, visa processing volume increased by 7%, total cross-border volume increased by 22% and transactions processed increased by 10%. We maintain our view that Visa is in a sweet spot as the company capitalizes on the trend toward a cashless society as well as the expansion of e-commerce.

Property light and free cash flow rich

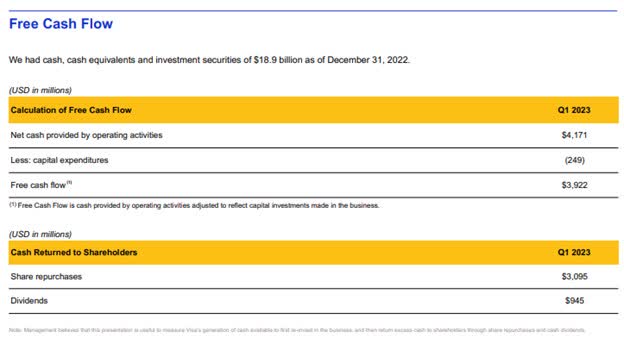

Visa is a free cash flow generator and is increasingly delinquent and fee free, unlike any other in the credit card space. (Image source: Visa)

Now let’s examine the finances. Visa is a capital-light entity, meaning that capital expenditures are very small relative to revenue and cash flow from operations. We are big fans of companies with such qualities as they are able to generate large amounts of free cash flow. Related to Visa, free cash flow in the fourth quarter came in at $3.92 billion, or 49 percent of total revenue. Visa’s business model is so cash-rich that for every $1 generated in revenue, approximately half is converted into free cash flow. Very few businesses have the characteristics of Visa’s profitability (ie operating margin and free cash flow profile), and we like the company and its growth prospects.

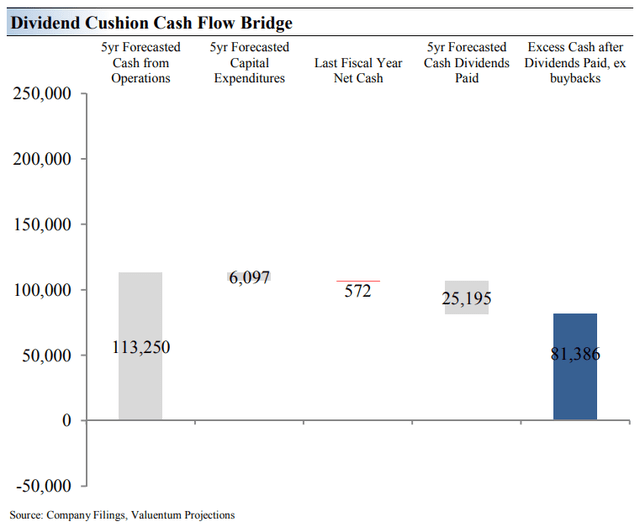

The growth potential of the Visa dividend is excellent. (Image Source: Valuentum)

As we’ve mentioned before, Visa is a free cash flow powerhouse, and as our cumulative five-year cash flow from operations and capital expenditure forecast in the figure above shows, we expect the company to have significant financial flexibility to grow or increase its dividend. Returning shareholders through acquisitions in the coming years. Visa’s big problem as a profit growth idea is that the profit margin is small at 0.8%. That compares to the average S&P 500 company’s dividend yield of ~1.6 percent. While it’s hard to like Visa, for a hobby that’s currently in short supply compared to other large multinationals, the company has plenty of room to raise its payout.

Concluding thoughts

Visa is one of our favorite companies for a long time. It leads to the global growth trend towards a cashless society and benefits from the expansion of e-commerce. The company’s operating margin is an easy sight to see, and its free cash flow margin is excellent. We expect Visa to generate significant free cash flow in the coming years and dividend growth will benefit from this. Based on the high end of the cash-flow-earned fair value range ($259 per share), the shares may have meaningful upside potential. We really like Visa, and we think it’s at least one on your radar.

This article or report and any links contained therein are for informational purposes only and should not be construed as a solicitation to buy or sell any security. VALUE IS NOT RESPONSIBLE FOR ANY ERRORS OR OMISSIONS OR RESULTS FROM THE USE OF THIS MATERIAL AND ACCEPTS NO LIABILITY FOR HOW READERS CHOOSE TO USE THE CONTENT. Estimates, opinions and estimates are based on our judgment on the date of the article and are subject to change without notice.

[ad_2]

Source link