[ad_1]

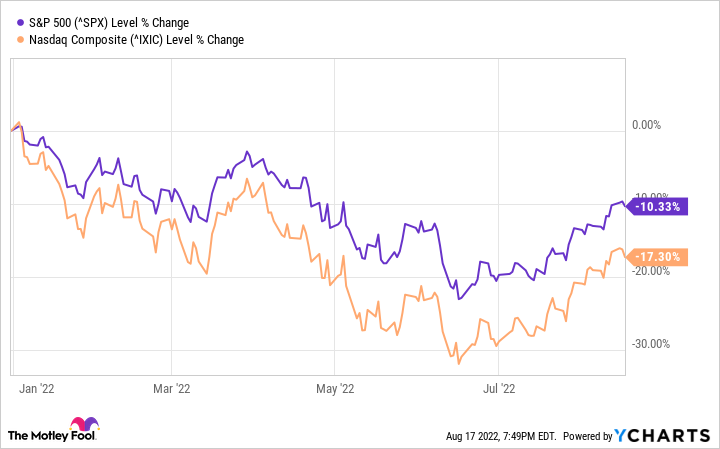

As of this writing, S&P 500 And Nasdaq Composite By 2022, the indices are down 10% and 17%, respectively. The global economy is slowing down, and some economists (and very loud market pundits) think a recession is likely this year and next. However, stocks have rebounded sharply from their mid-June lows.

Data by YCharts.

Has a new bull market begun or will a crash send stocks down? It’s hard to say. Either way, focusing on quality businesses that can grow despite macroeconomic issues is the way to go if you’re a long-term investor. Three Fool.com contributors think so Alphabet (GOOGL -2.46%) (GOOG -2.27%), LiveRamp Holdings (RAMP -1.71%)And Marvel Technology Group (MRVL -2.58%) Whatever happens next will grow. This is the reason.

This perpetual cash generator is being pushed by the CEO to improve further.

Billy Duberstein (Lyrics): Not sure which way the economy is going? Then it’s time to invest in companies with offensive and defensive qualities. And I can’t think of a better example than Google’s parent company, Alphabet.

On defense, Spell has three key features. First, Alphabet’s main search business is an effective monopoly in global search, with more than 91% market share as of last month.

Not only does Alphabet have a monopoly on search, but search itself is a pretty defensive business because it doesn’t require third-party data to effectively target ads. That’s in contrast to social media platforms that limited their targeting capabilities under IDFA privacy regulations last year. In a tough advertising environment, Google Search still grew 13.5% over the previous quarter, far outpacing its social media rivals, all of which struggled. When prospective customers enter their search terms, they are usually interested in purchasing a product. For this reason, search ads may be one of the last things advertisers hold back on ad spending.

Another defensive quality is Alphabet’s balance sheet, which has $125 billion in cash and only $14.7 billion in long-term debt. Alphabet has been ramping up its buybacks in recent years, so if the stock price falls or remains at low levels, management can retire that much stock without paying for growth opportunities. The company currently has a $70 billion buyback program, which could cut Alphabet’s stock 4.5% at today’s market price.

Third, Alphabet is a growing player in cloud computing. A latecomer with the third-highest market share, Alphabet’s Google Cloud Platform is still growing well, up 35.6% last quarter to a run rate of $19 billion. Because corporate customers generally save money and gain flexibility when switching to the cloud, the cloud computing industry as a whole should remain relatively stable even if the economy enters a recession.

On the flip side, if the economy improves, advertising budgets will increase. That’s not just search advertising, but Google’s ad networks and YouTube, which have been growing viewership, but have seen growth in advertising slow recently. Fidelity has invested heavily in artificial intelligence (AI) and new-age lunar capture, with projects that could see greater adoption if economic conditions improve. These include jobs in health data, fiber broadband and self-driving car company Waymo, among others.

Given the soft macroeconomic backdrop, CEO Sundar Pichai recently sent a companywide email: “We need to be more entrepreneurial, with greater urgency, stronger focus and more hunger than we’ve ever seen on a sunny day.”

Although Alphabet remains highly profitable and dominates the current environment better than others, Pichai is still pushing employees to work with less. That should make Alphabet an amazing defensive game.

LiveRamp deserves a very rich price tag

Anders Bylund (LiveRamp): Data management and analytics specialist LiveRamp Holdings offers a rare combination of strong growth and bargain-bin stock prices.

The company has close ties to the digital advertising market, where other businesses rely on its privacy-enhanced data collection and analysis tools to build and support their online marketing campaigns. Liveramp’s closest competitors tend to trade at sky-high valuations, often north of 20 times sales. But this stock has been thrown out with the market bathwater, changing hands today at 2.7 times sales.

At the same time, LiveRamp has more than doubled its sales in four years. Data-driven advertising is a hot topic and this company is a veteran in that field. As a result, the company crushed Wall Street estimates across the board in its most recently reported fiscal 2023 first quarter. However, the stock continues to sink to levels not seen since 2018, setting new multi-year lows.

LiveRamp’s high-margin software-as-a-service (SaaS) platform generates strong financial returns. The company has reported free cash flow of $56 million over the last four quarters, based on revenue of $552 million. LiveRamp’s balance sheet holds $508 million in cash and zero long-term debt. In addition, LiveRamp’s privacy-friendly data analytics platform is irreplaceable, which keeps its customers loyal.

In short, LiveRamp’s stock deserves double-digit price-to-sales ratios like the SaaS giant. Snowflake And Business deskBoth are close partners of Liveramp. Dollar-based net retention ratio pegged at 113% in the first quarter.

This stock is ready for an excellent restoration. If another failure is in the cards, LiveRamp’s return will only delay it to a reasonable valuation. If you are buying the stock at these bargain-bin prices, that looks like a profitable move.

The new-ish kid on the data center block

Nicolas Rossolillo (Marvel Technology Group) Everyone knows the names of top semiconductors Nivea And Advanced Micro Devices They are making heavy hay out of the fast-growing data center industry these days. But there are other chip companies getting a big lift from data center construction, AI and related technology activities. If you haven’t heard of it yet, let me introduce you to Marvel Technology Group.

Marvell has been designing chips for network infrastructure since the mid-1990s. Its data processing units (DPUs) are the heart of its semiconductor portfolio. These DPUs are specialized circuits responsible for moving and processing large amounts of data in a data center. Nvidia calls the DPU the “third pillar of the computing world,” along with central processing units (CPUs) and graphics processing units (GPUs).

Over the years, Marvell has steadily acquired smaller peers to expand into adjacent networking hardware such as data center switches, data storage controllers and Ethernet products. As a result, Marvell is now the leader in networking hardware for everything from AI to cybersecurity to automotive computing applications. While consumer electronics spending may face a cyclical downturn in the second half of 2022, data centers and adjacent markets such as 5G network infrastructure are still flying high. Most of Marvel’s revenue comes from these sources, not consumer products, so it can stay in growth mode.

For reference, Marvel posted sales of $1.45 billion in the first quarter of fiscal 2023, which ended April 30, and forecast very healthy sequential sales growth for Q2 ($1.515 billion in the midpoint of guidance). Management will report on Q2 on August 25. Prior to its quarterly report, Marvell stock traded at 41 times its enterprise value Earnings before interest, taxes, depreciation and amortization (EBITDA) is a premium price tag, but it’s improving rapidly as Marvel completes the results of two acquisitions in 2021. I am now a governor.

[ad_2]

Source link