[ad_1]

Adding business lines in the startup world is always a risk. A company can spread itself too thin and end up not doing a good job at anything. Or it may stumble upon an offering that not only hits but grows faster than its core product.

The latter appears to be true in Ramp’s case.

The beginning of the cost of the corporation The billing feature has started Building on the corporate card business and accounting software product in October 2021.

According to co-founder and CEO Eric Gleiman, within half a year of going public, Ramp has grown from operations to $1 billion in annual billings.

“The pace of growth has exceeded our company’s card business,” Gliman told TechCrunch in an interview. “It took us a very long time as a company to go from operating in the card business to $1 billion in annual volume. The pace and scale of adoption and how quickly businesses use the billing product is very fast.”

Originally, Billing was something existing customers could access and use for personal use. But as more people continue to use the feature, including paid providers, its popularity continues to grow.

“Now people are just coming in for a premium product,” Gleeman said.

The appeal, in his view, could be the ability to integrate with Ramp’s other offerings to a greater extent.

“When using a standalone solution like Bill.com, the user has to link that product to the accounting software and then link their credit card to the payment software so they can continue to run the accounting software on it,” Gleiman told TechCrunch. “Be able to manage automated accounting, expense management and invoice processing all in one platform with Ramp.

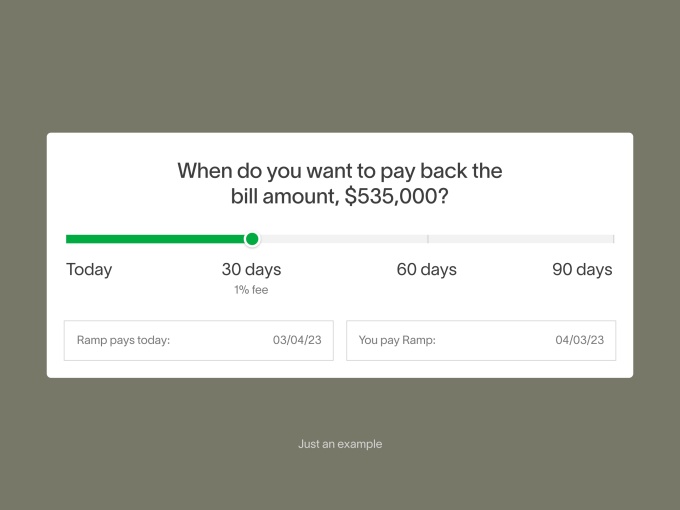

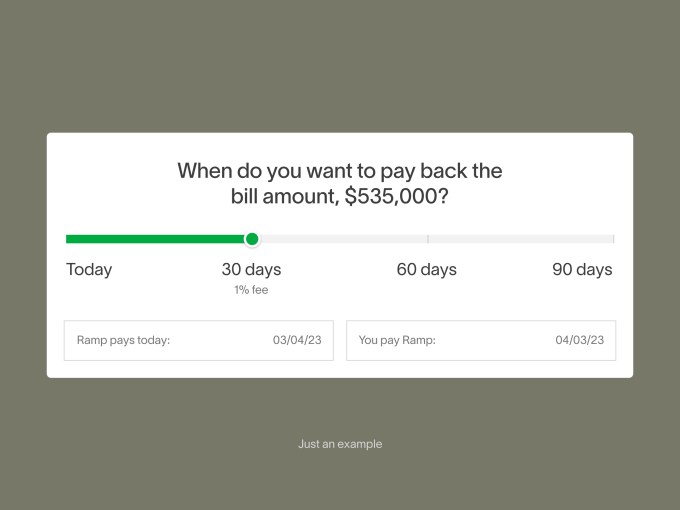

With the early success of the bill payment feature, Ramp is now adding financing and overlays it with a new product called Flex.

Initially, if a customer used Ramp to pay a vendor, they had 30 days to pay it back.

But with the new Flex feature, customers will have the “one-click” option to add financing to repay the loan in up to 30, 60 or 90 days. In addition to overtime, invoice payment gives businesses the flexibility to pay the way they want or the supplier wants, whether by ACH, check or card.

Image Credits: Ramp

“Many of the businesses we support have a lot of working capital. [when paying bills,]” said Gleeman. “Now you can extend financing through other forms of payment and support any invoice through us.”

The longer the financing term, the higher the fees paid by the business. Ramp earns money through the payment account by exchanging payments on those payments as well as when bills are paid. If the business doesn’t pay the money back within 30 days and they don’t use their card, Ramp doesn’t earn any money using the bill payment feature. But the thinking/hope behind it is that the software will bring in sticky customers.

Flex Available now to select customers. As part of the Ramp Early Access Program. The company “It’s actively working toward general availability in the next few months, though not in all US states.

The Flex feature appears to be an attempt to ramp up visibility in the increasingly crowded corporate spending space. Brax also has an invoicing feature that allows customers to transfer their bills and invoices to the originator for payment, or send them directly to their vendors. According to Ramp, customers can make payments to suppliers via ACH, wire or check. It does not charge any payment transaction fees, but does not indicate on its website that any flexible funding for those payments is provided through the ACH billing feature. Air Base and Rho also offer an invoicing feature, but there is no indication on their websites that they offer any financing through their bill payment feature via ACH.

In general, Gleiman anticipates that non-tech businesses — particularly those in industries such as e-commerce, construction and manufacturing — that have long cash-flow cycles and rely on working capital provisions beyond corporate cards will find the option to pay bills on a variable basis. “

“Now we can not only see if our customers’ bills are coming in, but we can help them decide how and when to pay,” Gleeman said.

In terms of overall revenue growth for the company, the nature of billing is becoming “very significant” in terms of the total amount of payments.

“We’re doing pretty well with billions of volumes on the cards,” Gliman said.

The move opens up the total addressable market (TAM) significantly for the ramp, suggesting that it is there Currently, $120 trillion in global B2B payments are made annually, of which only $1.5 trillion is by card.

“We are considering other avenues of expansion to make the product itself more valuable and drive adoption around core products,” he added.

But in today’s environment, isn’t Ramp worried about default risk?

Gleiman says the company is “not taking a leap or a new risk” with the new Flex feature. For example, if a business has a limit of $100,000, they can put $20,000 or $30,000 on their card and use that limit to offset some of the bill payments.

Overall, Ramp said, “he invested in really sophisticated credit risk and underwriting skills in the early days.”

“We even outperform our peer group with our current product,” Gliman told TechCrunch. “Flex will use the same underpinnings we use today for that core product.”

While Gliman did not disclose the company’s specific default price, he said he was “very excited.”

“Based on our understanding of the market, we believe we have an industry-leading performance in terms of our credit,” he said.

Of course, Ramp isn’t the only fintech startup expanding its offerings in an effort to become more competitive and one-stop shops for its customers. In the past few months, Brax has announced a “big push” into financial software with a focus on corporate customers, Airbus has announced it’s expanding its corporate card offerings, and Rho has said it’s adding expense management to its offerings.

Earlier this year, Ramp announced it was expanding into the travel business as well. In March, it raised $200 million in equity at a valuation of $8.1 billion.

[ad_2]

Source link