[ad_1]

solarseven

Domion Energy: A lot of fear on the business valuation

Dominion Energy, Inc.NYSE:D) is a leading integrated energy company with over 30 GW of electricity generation capacity. The company’s decision to conduct a “top-down business review”. It created panic among investors as they analyzed the impact on its future earnings power.

Utility investors generally dislike the unpredictability of earnings estimates, as utility stocks are considered more defensive instruments with less cyclical exposure to economic ups/downs. Therefore, they can maintain strong and predictable profit margins throughout the cycle, which we believe is critical to strengthening their valuation.

Therefore, Dominion Energy’s evaluation may not be liked by investors because CEO Bob Blue did not rule out that “the results of the evaluation will lead to different growth in terms of quality and quantity.” However, he believes it can provide “long-term value for our shareholders.”

Therefore, while investors are waiting for the results of the business evaluation, they may not be satisfied with the management’s view. In addition, as the macroeconomic situation worsens for the US economy, investors are anticipating a worse outcome that could have a significant impact on the projected 5Y consumption growth rate of 9% CAGR.

Dominion Energy: Wall Street is also shocked

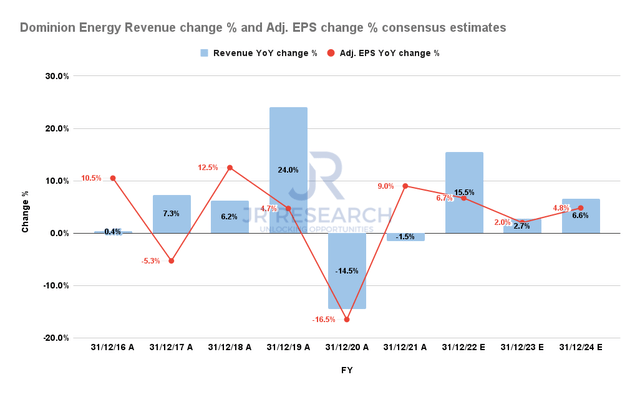

Dominion Energy’s Revenue Change % and Adj. EPS Change % Consensus (S&P Cap IQ)

Hence, even Wall Street analysts decided to lower the company’s FY23 adjusted EPS estimates to reflect such doubts. Accordingly, the revised estimates suggest an adjusted EPS increase of just 2%, well below the company’s “path to 6.5% EPS growth” in 2023. Investors should keep in mind that this amount is likely, pending the outcome of the trade review. danger.

We believe analysts’ pessimism is justified. If the business is doing well, there seems little reason to conduct a systematic review when there are significant macro headwinds. Therefore, we believe that D stock’s performance after its April 2022 peak reflects significant challenges for the company’s performance.

BoA said Dominion Energy’s “unique regulatory structure in Virginia” would affect its cash flow and could deprive it of further support for the review. Also, the performance bond litigation and settlement in Virginia has highlighted another concern for investors to consider.

But has the market’s tendency to discount the unknown reflected a significant headwind in the stock’s performance?

A: It can be a significant fear discount.

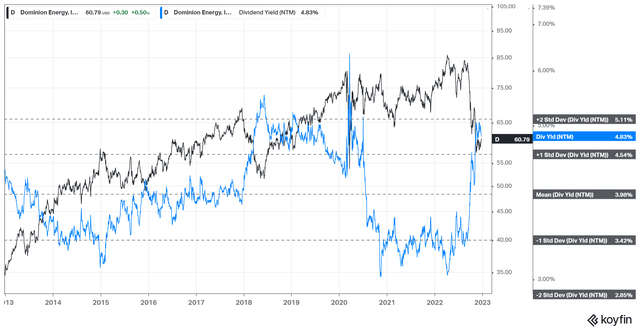

DNTM Dividend % yields a valuation trend (koyfin).

We think so. D last traded at NTM EBITDA of 9.2x, below the 10Y average of 12.2x. It is also below the peer median of 11.7x (based on S&P Cap IQ data). Additionally, NTM’s dividend yield of 4.83% rose to the two standard deviation zone above the 10Y moving average, confirming our belief that the market may be highly bearish.

There appear to be several red flags that investors should consider carefully when analyzing a company’s business valuation results. For example, is the company’s profit at risk? What about the cash flow drivers for the Virginia settlement?

In the year With the federal hawkish deadline until 2023, financing large investments in renewable energy, particularly offshore wind projects, may be more challenging. Therefore, investors should not avoid the additional impact on free cash flow, which will increase the uncertainty of the results of the business evaluation.

take away

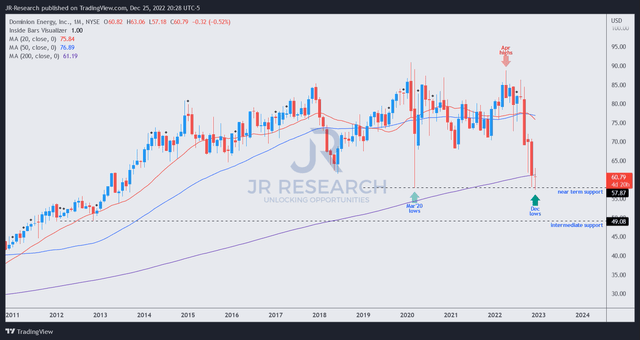

D Price Chart (Weekly) (TradingView)

Once again, we estimate that the bearish volume is blocked by the 200-month moving average (purple line) and finally made the low seen in March 2020. Given the fundamental challenges and technical downsides, we don’t expect D to recover significantly from here. However, we believe that a constructive consolidation zone is likely to emerge, which will help sustain the buying momentum for further recovery.

We therefore believe D’s price action reflects a significant hammering in the valuation, although the outcome of the business valuation is currently unknown. But if the review turns out to be better than feared, it will help lift the buying sentiment significantly.

Therefore, we believe that the current entry zone provides an opportunity for investors to get organized by incorporating risk-adjusted assumptions and assumptions.

Level: Buy

[ad_2]

Source link